Retirement used to feel simpler. You stopped working, your pension arrived, and taxes became someone else’s problem. In 2026, that picture has changed dramatically — and the numbers tell a story most retirees weren’t expecting.

The new state pension tax implications are shaping up as one of the biggest financial issues facing UK retirees this year. The full new State Pension has risen to almost the same level as the Personal Allowance. After the April 2026 increase, the full State Pension sits at £12,547.60 per year, while the Personal Allowance remains frozen at £12,570.

That leaves a tax-free buffer of just £22.40 annually.

In practical terms, even a small amount of savings interest, part-time earnings, or private pension income can now trigger a tax bill. Pensioners who never expected to pay Income Tax in retirement suddenly find HMRC letters landing on their doormats, PAYE codes shifting unexpectedly, or Simple Assessment notices arriving without warning.

This guide covers everything you need to understand:

- Whether the UK State Pension is taxable

- How HMRC collects tax from pensioners

- The triple lock state pension tax implications

- How savings and private pensions affect your liability

- Practical ways to reduce retirement tax surprises in 2026

Unlike most generic pension guides, this one also covers the “£22 buffer” in detail, the growing role of HMRC Simple Assessment letters, Scottish tax differences, and real-world examples pensioners are actually dealing with right now.

Is the UK State Pension Taxable in 2026?

Yes. The UK State Pension counts as taxable income — full stop.

The confusion usually starts because the State Pension arrives without tax being deducted first. The full amount lands directly in your bank account, which makes it feel tax-free. It isn’t. HMRC still counts every penny as taxable income, and the total gets added to everything else you earn.

Your State Pension combines with:

- Workplace pensions

- Private pensions

- Employment income

- Rental income

- Some savings interest

If the combined total exceeds your Personal Allowance, you owe Income Tax on the difference. According to GOV.UK’s official pension tax guidance, pension income is taxed under the same Income Tax rules as earnings from work — there’s no separate, gentler system for retirees.

Understanding how UK income tax bands work is the first step toward seeing how quickly pension income can become taxable in 2026.

The £22 Buffer: Why 2026 Is a Turning Point for Pensioners

The biggest retirement tax story in 2026 isn’t the triple lock itself. It’s what happens when rising pension payments collide with thresholds that haven’t moved in years.

| 2026/27 Figure | Amount |

|---|---|

| Full New State Pension (weekly) | £241.30 |

| Full New State Pension (annual) | £12,547.60 |

| Personal Allowance | £12,570 (frozen) |

| Remaining Tax-Free Buffer | £22.40 |

That £22.40 gap is razor-thin. A few pounds of savings interest. A small private pension. Occasional freelance income. Any of these can now push a pensioner’s total income over the threshold and into a tax liability they weren’t planning for.

For years, retirees comfortably sat below the tax threshold without any active planning. In 2026, millions are drifting into the tax system without becoming meaningfully wealthier — purely because pension payments rose while the allowance stayed put. That’s why questions about when the Personal Allowance will increase have become so pressing for retirees, not just workers.

How the Gap Has Narrowed Year by Year

To grasp how quickly this situation developed, look at the trajectory over recent tax years:

| Tax Year | Full State Pension | Personal Allowance | Remaining Gap |

|---|---|---|---|

| 2021/22 | ~£9,339 | £12,570 | ~£3,231 |

| 2022/23 | ~£9,628 | £12,570 | ~£2,942 |

| 2023/24 | ~£10,600 | £12,570 | ~£1,970 |

| 2024/25 | ~£11,502 | £12,570 | ~£1,068 |

| 2025/26 | ~£11,973 | £12,570 | ~£597 |

| 2026/27 | £12,547.60 | £12,570 | £22.40 |

Five years ago, there was a comfortable £3,000-plus cushion. Today it’s essentially gone. That’s not an accident — it’s the direct result of the triple lock working as designed, while tax thresholds stay frozen.

Triple Lock State Pension Tax Implications Explained

The triple lock was designed to protect pensioners from inflation by increasing the State Pension each year by whichever is highest: inflation, average earnings growth, or 2.5%. In 2026, the rise linked to earnings growth produced a significant uplift in payments.

The problem is structural. The triple lock pushes pension income upward every year. The Personal Allowance doesn’t move. The result is a slow but accelerating process called fiscal drag — sometimes described as a stealth tax — where the government doesn’t technically raise rates, but more income becomes taxable simply because thresholds stand still while incomes rise.

For pensioners, this produces three very practical consequences:

- More PAYE adjustments arriving mid-year

- More HMRC tax notices and Simple Assessment letters

- Smaller effective increases than the headline triple lock figure suggests

The question of whether Labour will increase the Personal Allowance has become central to retirement planning discussions in 2026, because without that move, fiscal drag will continue pulling more pensioners into the tax system every single year.

Why Your “Tax-Free” Pension May Still Create a Tax Bill

Many retirees assume: “If tax isn’t deducted from my State Pension, I must not owe any.” That assumption is incorrect — and it’s exactly the misunderstanding that leads to nasty surprises.

The State Pension arrives gross, without deductions. HMRC then collects any tax owed through PAYE tax code adjustments on a workplace or private pension, direct billing via Simple Assessment letters, or — in some cases — a formal P800 tax calculation.

Example: How Pension Tax Builds Up

| Income Source | Annual Amount |

|---|---|

| New State Pension | £12,547.60 |

| Small Workplace Pension | £3,500 |

| Savings Interest | £400 |

| Total Income | £16,447.60 |

Taxable income calculation: £16,447.60 − £12,570 = £3,877.60 taxable at the basic rate. On that example alone, the tax owed is around £775 — money many retirees simply haven’t budgeted for.

Why Some Pensioners Receive Unexpected HMRC Tax Letters

Picture this: you receive your full pension every month, budget accordingly, and then a letter from HMRC arrives six months later demanding several hundred pounds in unpaid tax. That situation is becoming increasingly common in 2026 — and it catches people completely off guard.

The Simple Assessment System Explained

For pensioners who owe tax but don’t submit Self Assessment tax returns, HMRC uses a process called Simple Assessment. Rather than asking you to file a return, HMRC calculates what it believes you owe and sends either a P800 tax calculation or a Simple Assessment letter (PA302).

This typically happens when State Pension income rises above the threshold, PAYE codes fail to update quickly enough, savings interest increases during the year, or multiple pensions complicate the picture.

Many pensioners don’t realise they owe anything until these letters land. If you receive one, don’t ignore it — but also don’t pay immediately without checking the figures against your own records. HMRC tax bill errors do happen, and pensioners with multiple income streams are particularly exposed to miscalculations.

Does HMRC Handle It Automatically?

Usually, yes. In many cases, HMRC adjusts your tax code, deducts tax from another pension you receive, or requests payment through Simple Assessment directly. But checking your PAYE code at least once a year is still essential — retirement transitions create coding mistakes more often than most people realise. If something looks off, checking your tax code should be the first move before contacting HMRC.

Human Tip — Don’t Wait for the Letter

HMRC’s systems don’t always catch pension tax liability in the same tax year it arises. If you started receiving a new pension income stream during 2025/26 and your PAYE code hasn’t updated to reflect it, log into your Personal Tax Account on GOV.UK and check whether your coding notice accounts for all income sources. A proactive check now is far less painful than a surprise bill in twelve months.

The Savings Interest Trap Catching Pensioners in 2026

Higher interest rates helped savers earn better returns on cash deposits — but they created a new tax problem for retirees at the same time. With the Personal Allowance buffer now essentially gone, even modest savings interest can tip a pensioner into taxable territory.

| Income Type | Amount |

|---|---|

| State Pension | £12,547.60 |

| Savings Interest | £350 |

| Total Income | £12,897.60 |

Even without a private pension in this example, taxable income now exists. This is one reason so many pensioners are entering HMRC’s tax system for the first time in years — not because their circumstances changed dramatically, but because the numbers stopped working in their favour.

There’s a detailed breakdown of how savings interest tax works and where the hidden bite lands — worth reading before assuming your Personal Savings Allowance covers everything. And if you’re monitoring your savings accounts carefully this year, you may also want to check whether HMRC’s tax crackdown on savings accounts affects how your interest is being reported.

State Pensioners: Tax Implications If You Still Work

More retirees are continuing in part-time work beyond State Pension age, driven by rising living costs. The tax reality is that employment income and pension income combine — HMRC doesn’t separate them.

| Income Source | Amount |

|---|---|

| State Pension | £12,547.60 |

| Part-Time Job | £14,000 |

| Total Income | £26,547.60 |

At that combined level, around £13,977 is taxable, producing a tax bill of roughly £2,795 at the basic rate. This may increase PAYE deductions from the employment income, reduce Personal Savings Allowances, and potentially push some working pensioners closer to the higher-rate band.

For any retiree holding a second income source alongside their pension, understanding how second job tax works in the UK is directly relevant — the same principle applies when pension income fills most of the personal allowance before employment income is even added.

Interestingly, Germany recently introduced tax breaks specifically for working pensioners — a contrast worth noting as UK policy heads in the opposite direction through threshold freezes.

Scottish Pensioners Face Different Tax Rules

Pensioners living in Scotland should remember that Scottish Income Tax bands diverge from the rest of the UK. The Personal Allowance remains UK-wide, but Scotland applies different starter, basic, and intermediate rates beginning at 19%.

For retirees near tax thresholds, even small regional differences can affect take-home income from employment earnings, private pension withdrawals, and combined retirement income. If you’re a Scottish pensioner unsure which band applies to your situation, the Scottish tax brackets guide breaks this down clearly.

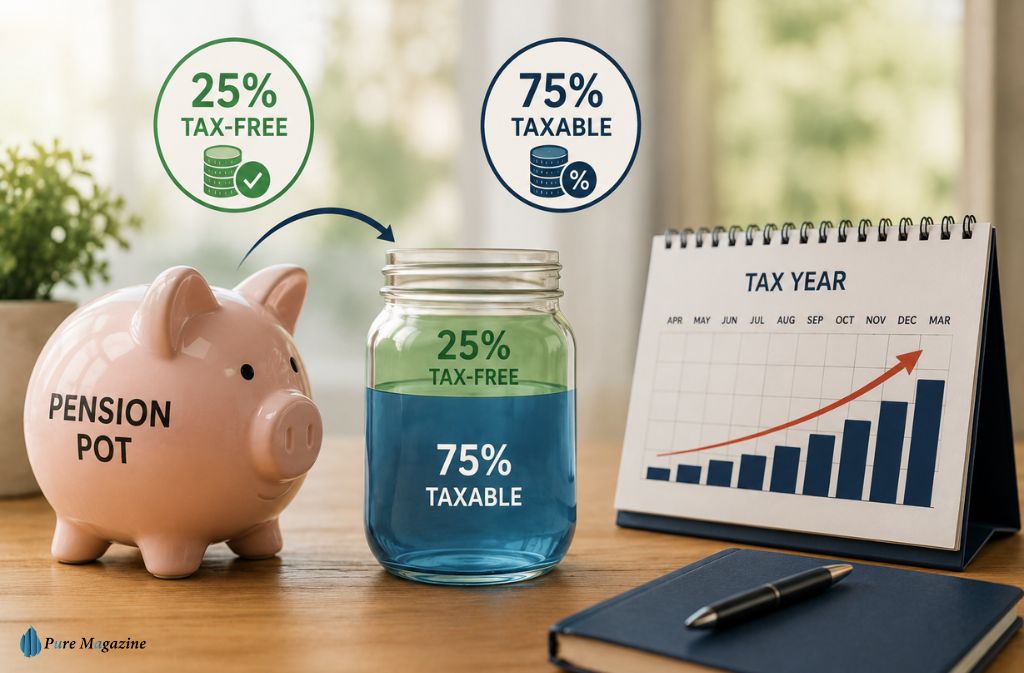

How Much of Your Pension Can You Take Tax-Free?

Most private pensions still allow up to 25% tax-free as a lump sum, with the remaining 75% treated as taxable income. That rule hasn’t changed — but the way large withdrawals interact with other pension income is catching more people out in 2026.

| Pension Withdrawal | Tax Treatment |

|---|---|

| First 25% | Usually tax-free |

| Remaining 75% | Taxable as income |

A large withdrawal in a single year can accidentally push retirees into a higher tax band or trigger a much bigger HMRC bill than expected. Many pensioners now spread withdrawals across multiple tax years to reduce this effect — and it’s a strategy worth discussing with a financial adviser before making any large pension decision.

There have also been discussions about whether the 25% tax-free lump sum could be scrapped in future budgets. Nothing is confirmed, but if you’re planning a withdrawal, understanding the current rules — and potential changes — matters. You should also review what happens with inheritance tax on pension funds if you’re not planning to draw everything down, as the rules here shifted significantly with HMRC’s inheritance tax changes heading toward 2027.

Watch Out: The Pension Withdrawal Spike

Taking a large taxable pension withdrawal in the same tax year you begin receiving the full State Pension is one of the most common ways retirees end up in a higher tax band unexpectedly. The State Pension uses almost all of your Personal Allowance before the withdrawal is even considered. Plan withdrawals with the full income picture in view.

The Retirement Tax Pressure Framework

Retirement taxes feel confusing because several income streams — each one seemingly manageable — combine into something much larger. The easiest way to understand the total pressure is through this framework:

- State Pension — Now uses almost the entire Personal Allowance. Any other income is effectively taxed from pound one.

- Private or Workplace Pensions — These become largely taxable once the allowance is absorbed. Even modest amounts produce a tax liability.

- Savings Interest — Matters far more than it did three years ago because the remaining buffer is so small. £300 in interest can now mean a tax bill.

- Extra Income — Part-time work, rental income, freelance earnings, or investment income can rapidly push total taxable income into territory that triggers both higher deductions and potential HMRC notifications.

Individually, none of these streams sounds alarming. Together, they can produce a tax bill that arrives as a genuine shock — particularly for retirees who haven’t revisited their income picture since the previous tax year.

Common Pension Tax Mistakes in 2026

Assuming the State Pension is automatically tax-free. It’s taxable income even though the deductions aren’t visible in the payment itself. The tax comes later — usually through PAYE or a letter.

Ignoring savings interest. Small amounts matter now in a way they simply didn’t three years ago. If your bank pays you anything meaningful, factor it into your income total.

Taking large pension withdrawals at once. This can trigger unnecessarily higher-rate tax liabilities in a single year. Spreading withdrawals is almost always more tax-efficient.

Forgetting to check PAYE codes. Retirement transitions — particularly starting a new pension stream or changing employment status — frequently create coding errors. A wrong tax code during retirement can mean overpaying for months before anyone catches it.

Trusting HMRC to calculate everything perfectly. PAYE errors involving multiple pensions are common. If you receive more than one pension payment, check that each provider holds the right code. The HMRC pension tax code rule change introduced new complexities that are still being worked through the system.

How to Reduce Tax in Retirement Legally

Retirement tax planning is becoming just as important as retirement saving — and the strategies available are straightforward once you know where to look.

Spread pension withdrawals across tax years. Avoid large taxable lump sums in a single year whenever possible. Two smaller withdrawals in consecutive years nearly always produce a lower combined tax bill than one large one.

Use ISAs strategically. ISA income doesn’t count toward Income Tax thresholds. If you hold cash savings or investments that generate interest, moving them into an ISA wrapper removes them from the taxable income calculation entirely. The full guide to how ISAs work explains the options — and a Cash ISA with HMRC’s rules in mind is particularly relevant for retirees holding large cash balances.

Review PAYE codes every year. Especially after pension increases, new pension income streams, or any change in employment status. Small errors compound quickly.

Consider the Marriage Allowance. If one partner’s income sits below the Personal Allowance, transferring part of it to the higher-earning spouse can reduce the overall tax bill.

Monitor total taxable income as a single figure. Looking at each stream separately hides the combined picture. Run the full calculation — State Pension plus all other income minus the Personal Allowance — at least once before each tax year-end.

If you’ve overpaid tax in previous years through incorrect codes or underclaimed relief, it’s also worth checking whether you have any unclaimed tax refunds sitting with HMRC — many retirees discover they’re owed money once they look.

State Pension Age Began Rising in 2026

A separate but related change: the UK State Pension age began its gradual increase from 66 to 67 in April 2026. This transition will continue over several years and determines when future retirees can first claim the State Pension.

For workers approaching retirement, this means longer working lives, delayed pension access, and potentially more years paying Income Tax before retirement income begins. It also raises the stakes on pension forecasting and retirement income planning — because the gap between stopping work and receiving State Pension income may now be longer than previously expected.

Understanding how much you can earn before paying tax becomes especially relevant during that bridge period, when employment income may combine with private pension withdrawals before the State Pension kicks in at all.

Quick Pension Tax Cheat Sheet

| Question | Short Answer |

|---|---|

| Is the UK State Pension taxable? | Yes |

| Is tax deducted automatically from the State Pension? | Usually no |

| Is the full State Pension below the Personal Allowance? | Barely — by just £22.40 |

| Can savings interest trigger tax? | Yes, even small amounts |

| Do working pensioners pay Income Tax? | Often yes |

| Can HMRC send tax letters automatically? | Yes — P800 or Simple Assessment |

| Is 25% of a private pension tax-free? | Usually yes |

| Does Marriage Allowance help? | Yes, for eligible couples |

FAQs

Yes. The UK State Pension is taxable income. Although tax is not deducted before payment, HMRC may collect tax through PAYE adjustments, pension tax codes, or Simple Assessment letters if your total income exceeds the £12,570 Personal Allowance.

Q. Is the UK State Pension taxable in 2026?

Yes. The UK State Pension counts as taxable income in 2026, even though payments are made without automatic tax deductions.

Q. Why are more pensioners paying tax in 2026?

The full new State Pension rose to £12,547.60 in 2026 — just £22.40 below the frozen Personal Allowance. Even small extra income can now trigger tax.

Q. Do I need to contact HMRC if my State Pension becomes taxable?

Usually not. HMRC often adjusts your PAYE tax code automatically or sends a P800 or Simple Assessment letter explaining any tax owed.

Q. Can savings interest make my pension taxable?

Yes. Savings interest can push total income above the Personal Allowance, especially now that the State Pension sits so close to the tax threshold.

Q. Is State Pension taxed at source?

No. The State Pension is paid gross without tax deductions. HMRC usually collects tax through PAYE adjustments or direct billing.

Q. Can I work while receiving the State Pension?

Yes. Employment income and State Pension income combine for tax purposes, which may increase your Income Tax liability.

Q. How much of my private pension can I take tax-free?

Most private pensions allow up to 25% as a tax-free lump sum. The remaining withdrawals are usually taxable.

Q. What is HMRC Simple Assessment?

Simple Assessment is a system where HMRC calculates unpaid tax automatically and sends pensioners a bill without requiring a Self Assessment return.

Q. Does Marriage Allowance help reduce pension tax?

Yes. Eligible couples may transfer part of an unused Personal Allowance to reduce their household tax bill.

Conclusion

The new state pension tax implications in 2026 are affecting far more retirees than most people expected. Triple lock increases and frozen tax thresholds have combined to leave the full new State Pension just £22.40 below the Personal Allowance — a gap so small that savings interest alone can close it.

The biggest mistake pensioners make is treating each income stream in isolation. HMRC looks at the whole picture: State Pension, workplace pensions, private pensions, savings interest, and employment income. When you add those together, the tax position looks very different from what any single figure suggests.

Understanding how PAYE adjustments, Simple Assessment letters, pension withdrawals, and savings income interact can help you avoid nasty surprises and plan retirement income more efficiently. You can also check how much income tax you’ve already paid through your Personal Tax Account — a useful starting point before assessing whether your current tax position is correct.

With pension income now so close to the tax threshold, staying on top of your numbers isn’t optional anymore. It’s just part of managing retirement in 2026.

For more guides on UK tax, pensions, and personal finance, visit Pure Magazine.