|

TL;DR — Key Takeaways for Over-55s (2026)

|

The Tax Problem Nobody Warned You About

Martin and Elaine were both 68, mortgage-free, and quietly confident they’d done everything right. They’d saved steadily, avoided risky investments, and never thought of themselves as “wealthy.”

Then their solicitor paused, rechecked the numbers, and explained that their children could be facing an inheritance tax bill of nearly £100,000 — largely because their house had increased in value.

We’re seeing this shift on the ground more and more. Not reckless spending. Not tax avoidance. Just ordinary over-55s drifting into an inheritance tax problem they never planned for.

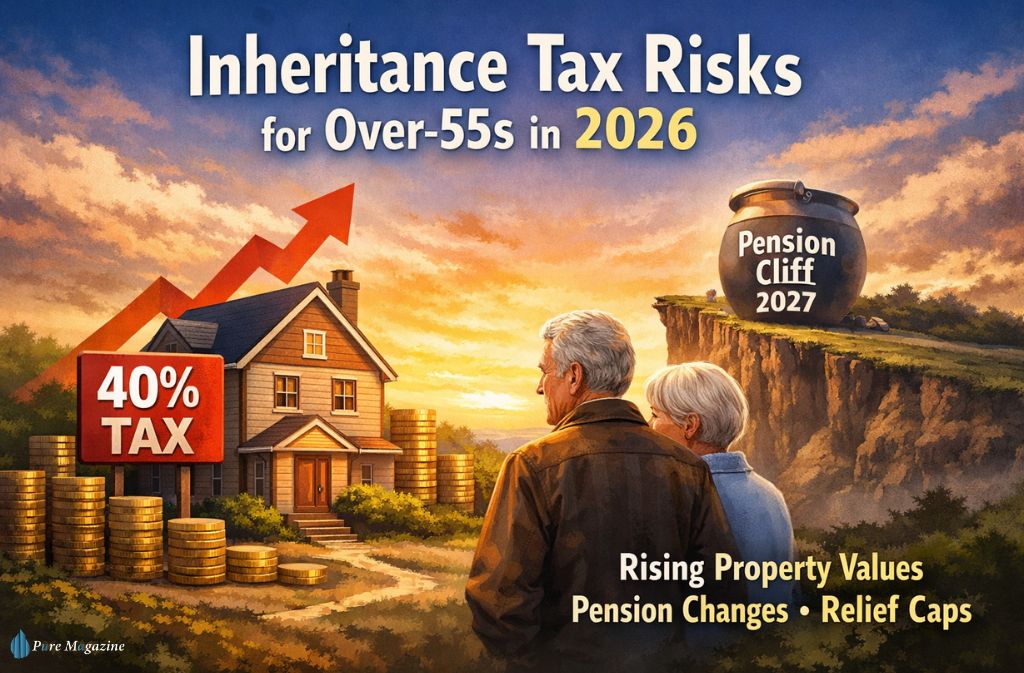

If you’re over 55, inheritance tax risk in 2026 looks very different from what it did even ten years ago. This guide explains why, what’s changing next, and how families can still act — calmly and legally — before options narrow.

The 2026 “Triple-Threat” to Family Legacies

Answer-first summary:

In 2026, the primary inheritance tax risk for over-55s isn’t wealth — it’s the combination of frozen thresholds, rising asset values, and upcoming pension rule changes that inflate estates above the tax line without families noticing.

1. The Boiling Frog Threshold Freeze

Inheritance tax feels like a boiling frog problem. The tax rate hasn’t changed, but the water keeps getting hotter.

The £325,000 inheritance tax threshold has been frozen for years. Meanwhile, property prices — especially in London and the South East — have continued to rise. Families don’t feel the pressure building until the bill lands after death, when there’s no room left to manoeuvre.

Why this matters:

You can become “IHT-exposed” without earning more, saving more, or changing your lifestyle at all.

Authority snapshot

| Factor | 2015 | 2026 |

|---|---|---|

| Inheritance Tax Threshold | £325,000 | £325,000 |

| Average UK House Price | ~£190,000 | £285,000+ |

| Estates Affected by IHT | Minority | Growing middle class |

2. The Pension Cliff (Looking Ahead to 2027)

For years, pensions were treated as the safest inheritance tax shelter. Many over-55s planned to live off other assets and leave pensions untouched for their children.

That assumption is now fragile.

From April 2027, under current proposals, unused pension funds are expected to be brought into the inheritance tax estate. This would fundamentally change estate planning for retirees.

Will my pension be subject to inheritance tax after 2027?

Possibly. If unused pensions are included in your estate:

- Larger estates may cross the IHT threshold unexpectedly

- Pension-heavy families could face liquidity problems

- Old beneficiary nominations may create unintended outcomes

This is now the number-one concern for many over-55s reviewing their plans.

3. Relief Caps Most People Miss

The £2m Residence Nil-Rate Band Taper (The Silent Killer)

Many homeowners assume the residence nil-rate band automatically protects their home. It doesn’t.

Once your estate exceeds £2 million, the residence nil-rate band is withdrawn at a rate of £1 for every £2 over the limit. For property-heavy estates, this can erase the allowance.

This catches people who:

- Bought modest homes decades ago

- Live in high-growth areas

- Never felt “rich” during their lifetime

How does the 2026 IHT cap affect my family business?

In 2026, 100% Business Property Relief and Agricultural Relief are capped at £2.5 million. Any excess may face inheritance tax at up to 40%.

For family businesses and farms, this creates a new risk:

The business may survive — but the cash to pay the tax may not.

The Most Common Inheritance Tax Mistakes Over-55s Make

- Assuming inheritance tax is only for the wealthy

- Putting a house in children’s names (triggering gift-with-reservation rules)

- Leaving pension nominations untouched for decades

- Making large gifts too late for the 7-year rule to help

- Not reviewing wills after remarriage or property moves

Doing nothing is now one of the most expensive mistakes.

Also Read: HMRC Inheritance Tax Changes 2027: How to Protect Your Pension & Family Wealth

The 7-Year Gifting Rule (And What Taper Relief Actually Means)

Many people misunderstand how taper relief works.

| Years Between Gift & Death | IHT Due |

|---|---|

| 0–3 years | 40% |

| 3–4 years | 32% |

| 4–5 years | 24% |

| 5–6 years | 16% |

| 6–7 years | 8% |

| 7+ years | 0% |

Important:

Taper relief reduces the tax, not the value of the gift. The full amount still counts toward your estate calculation.

Case Study: How “Ordinary” Families Get Caught

Profile

- A couple aged 67 and 69

- Home value: £550,000

- Savings & investments: £220,000

- Pension funds: £400,000

Without planning

- Estate exceeds allowances

- Estimated inheritance tax: £96,000

That £96,000 isn’t an abstract figure. It’s a grandchild’s first home deposit — or a decade of university fees — lost simply because no one joined the dots early enough.

With structured planning

| Scenario | Estimated IHT |

|---|---|

| No planning | £96,000 |

| Basic allowances used | £58,000 |

| Structured planning | £18,000–£25,000 |

When Inheritance Tax Planning Still Works (And When It Doesn’t)

Ages 55–65

- Maximum flexibility

- Gifting strategies still powerful

- Pension and trust planning viable

Ages 65–75

- Options narrow

- Focus shifts to structure and sequencing

- Residence nil-rate band planning is critical

Age 75+

- Damage limitation

- Liquidity planning for heirs

- Avoiding rushed decisions becomes the priority

A Simple IHT Risk Estimator (Illustrative)

| Estate Value | Est. Tax (No Planning) | Est. Tax (With Planning) |

|---|---|---|

| £600,000 | £40,000 | £0 |

| £1,000,000 | £200,000 | £80,000 |

| £1,800,000 | £520,000 | £260,000 |

Figures vary by circumstance, but the pattern is consistent: early action matters more than aggressive tactics.

Checklist: Are You at Risk?

- ⬜ Over 55 and own property

- ⬜ Estate likely above £500,000

- ⬜ Pension nominations older than 5 years

- ⬜ No recent will review

- ⬜ No gifting or estate strategy

If you tick two or more, inheritance tax exposure is likely.

Also Check: Inheritance Tax When the Second Parent Dies – What Families Discover Too Late

What Might Change Next?

- Continued threshold freezes

- Greater scrutiny of pension death benefits

- Further limits on reliefs

- Increased use of digital estate reporting

Inheritance tax is becoming more structural, not temporary.

FAQs

Q. How much can you inherit tax-free in the UK?

In the UK, you can inherit up to £325,000 tax-free under the standard inheritance tax threshold. This can increase to £500,000 if a main residence is passed to direct descendants and the residence nil-rate band applies. Married couples and civil partners may pass on up to £1 million tax-free if allowances are fully transferable.

Q. How can I legally avoid paying 40% inheritance tax?

You can legally reduce or avoid the 40% inheritance tax rate by using available allowances, structured lifetime gifting, spousal exemptions, and careful pension planning. The key is acting early — last-minute transfers and aggressive schemes often fail under HMRC rules.

Q. Can I give my house to my children to avoid inheritance tax?

Usually not. If you give your house to your children but continue living in it, HMRC treats this as a gift with reservation of benefit, meaning the property still counts as part of your estate for inheritance tax purposes. This is one of the most common inheritance tax mistakes.

Q. Will my children have to pay inheritance tax on my house?

Your children may have to pay inheritance tax on your house if the total value of your estate exceeds the available allowances. Whether tax is due depends on property value, other assets, marital status, and whether the residence nil-rate band applies.

Q. Is inheritance tax unavoidable in the UK?

Inheritance tax is not always unavoidable, but avoiding it requires early and informed planning. Many families reduce or eliminate inheritance tax exposure through allowances, gifting strategies, and estate planning — often years before tax becomes due.

Q. Do pensions count towards inheritance tax in the UK?

Currently, pensions may fall outside the inheritance tax estate, depending on their structure and the age at death. However, from April 2027, unused pension funds are expected to be included more broadly for inheritance tax purposes, significantly increasing inheritance tax risk for over-55s.

Q.At what point should over-55s start inheritance tax planning?

Ideally, inheritance tax planning should begin between the ages of 55 and 65, when gifting rules, pension planning, and allowances are most effective. Waiting until later can severely limit available options.

Conclusion

Inheritance tax planning for over-55s in 2026 isn’t about clever loopholes. It’s about recognising how quietly the system has changed — and how easily sensible families can be caught out.

Frozen thresholds, rising property values, pension rule changes, and relief caps mean inheritance tax risk now affects far more people than ever before. The earlier you acknowledge that shift, the more options you keep.

If you’re over 55, the window for calm, effective planning is still open — but it doesn’t stay that way forever.

Related: Deed of Variation Inheritance Tax Avoidance 2026

Accuracy note: This guide reflects UK inheritance tax rules and HMRC guidance as of February 2026, including changes under the Finance Act 2025 and subsequent consultations. Tax rules can change, and individual circumstances vary.