Tax-efficient investing in the UK shifted significantly in April 2026 — and most articles still haven’t caught up with what actually changed.

While many investors still treat EIS as a niche strategy, the latest reforms widened access to larger, more established companies, restructured the rate between EIS and VCT, and locked the scheme in through 2035. That combination matters more than any single headline figure.

This guide covers how EIS tax relief works in 2026, what changed from 6 April, and why it matters — including the paperwork realities, loss scenarios, and carry-back strategy that rarely get mentioned.

What Is EIS Tax Relief?

EIS tax relief is a UK government incentive allowing investors to reduce income tax, defer capital gains tax, and limit downside risk when putting money into qualifying early-stage companies. The scheme channels capital into high-growth UK businesses that struggle to raise funding through conventional routes.

In simple terms: you invest, the government shares part of the risk, and qualifying companies get access to capital they couldn’t easily find elsewhere.

Understanding how EIS fits alongside other tax-efficient structures — from ISAs to pension contributions — is the starting point for building an efficient investment strategy in 2026.

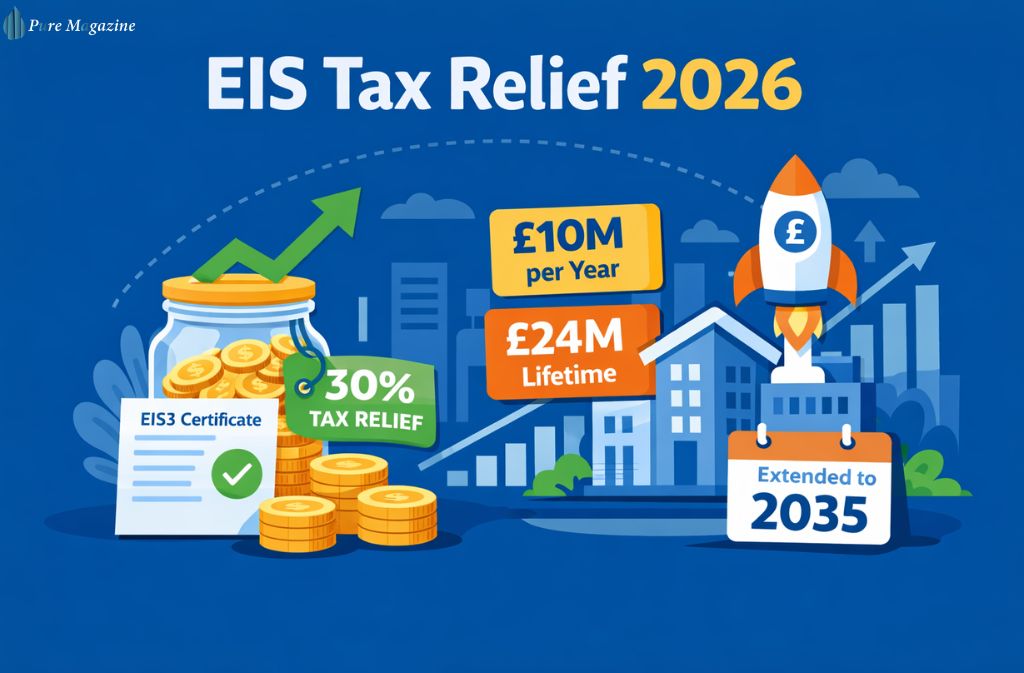

What Changed from 6 April 2026?

1. The Company Limit Hike

As confirmed by Saffery’s February 2026 analysis of the EIS and VCT changes, the company-side thresholds doubled from 6 April 2026:

| Limit | Before April 2026 | From April 2026 |

|---|---|---|

| Annual company raise (EIS) | £5m | £10m |

| Annual company raise (KIC) | £10m | £20m |

| Lifetime company cap (EIS) | £12m | £24m |

| Lifetime company cap (KIC) | £20m | £40m |

| Gross assets before investment | £15m | £30m |

| Gross assets after investment | £16m | £35m |

These changes mean EIS now supports scaling companies — not just tiny startups — which typically carry lower failure rates and stronger exit potential.

2. The Rate Split: What Actually Changed

This is the most important correction that most articles get wrong. As RJP’s January 2026 analysis confirms, VCT income tax relief dropped from 30% to 20% from 6 April 2026. EIS income tax relief stays at 30% — but only for investments under the original lower company limits. Companies accessing the new higher limits (£10m annual / £24m lifetime) fall under a restructured regime where certain provisions differ.

For most individual investors putting up to £1 million into standard EIS-qualifying companies, the 30% rate remains intact. The rate divergence makes EIS considerably more attractive relative to VCT for high earners in 2026:

| Feature | EIS | VCT (from April 2026) |

|---|---|---|

| Income tax relief | 30% | 20% |

| CGT-free gains (3+ years) | Yes | Yes |

| Loss relief against income | Yes | No |

| Inheritance tax relief (2+ years) | Potentially | No |

That 10-percentage-point gap is pushing higher earners toward EIS — particularly those who’ve already used their ISA allowance and are looking for the next layer of tax-efficient positioning.

3. The Sunset Clause Extension

The scheme is now secured through 2035. Before this extension, uncertainty about the scheme’s continuation created hesitation among investors thinking in five-to-ten year horizons. Long-term planning is now viable in a way it wasn’t previously.

How EIS Tax Relief Works: The Four Layers

1. Income Tax Relief (30%)

You claim back 30% of your investment directly against your income tax bill. As GOV.UK’s venture capital schemes guidance confirms that you can invest up to £1 million annually (£2 million if at least £1 million goes into Knowledge-Intensive Companies), and you must have sufficient income tax liability to absorb the relief.

| Investment | Income Tax Relief | Real Net Cost |

|---|---|---|

| £10,000 | £3,000 | £7,000 |

| £50,000 | £15,000 | £35,000 |

| £100,000 | £30,000 | £70,000 |

Unused relief cannot be carried forward — but it can be carried back to the previous tax year, which creates a strategic timing lever covered below.

2. Capital Gains Tax Deferral

Reinvesting a capital gain into EIS defers the CGT liability until the EIS shares are sold. The gain can come from any source — property disposals, share sales, or crypto realisation. The disposal must have occurred within 12 months before the EIS investment or within 36 months after it.

For anyone sitting on a significant gain, this deferral mechanism turns an EIS investment into a tax management tool as much as an investment vehicle. How much capital gains tax you’d otherwise owe determines how valuable that deferral actually is.

3. Tax-Free Growth

Hold EIS shares for at least three years, and any capital gain on disposal is completely exempt from CGT. On a £20,000 investment that grows to £50,000, the £30,000 profit is entirely yours.

4. Loss Relief: The Real Safety Net

This is where experienced EIS investors think differently from beginners.

If an EIS investment fails, you can offset the net loss — after deducting the income tax relief already received — against income tax. For a 45% taxpayer, the effective maximum risk on any failed investment looks like this:

| Investment | 30% income tax relief | Net cost | If total loss, offset at 45% | Real loss |

|---|---|---|---|---|

| £10,000 | £3,000 | £7,000 | £3,150 | £3,850 |

A 45% taxpayer effectively risks around 38.5p per £1 invested on a complete write-off. That’s why sophisticated investors treat EIS as a heavily cushioned bet on high-growth companies — not risk-free, but with the downside meaningfully absorbed by the tax structure. Understanding how the 40% and 45% tax brackets work makes this calculation concrete for your own position.

A Real EIS Scenario

| Stage | Amount |

|---|---|

| Investment | £20,000 |

| Income tax relief (30%) | £6,000 |

| Net cost | £14,000 |

| Exit value after 3 years | £50,000 |

| CGT on £30,000 gain | £0 |

| Net profit | £36,000 |

The income tax relief reduces the effective base cost, and the CGT exemption means the full exit value is retained. The after-tax calculator can help model how much income tax liability you’d need to absorb the full 30% relief at different investment sizes.

EIS Rules and Eligibility (2026)

Investor requirements:

- UK taxpayer with sufficient income tax liability

- Not “connected” to the company (cannot hold more than 30% of shares, or be an employee)

- Must hold shares for at least three years

Company requirements:

- UK-based with a permanent establishment here

- Carrying on a qualifying trade (not investment-focused)

- Must have made its first commercial sale within seven years (ten years for KICs)

- Under 250 full-time employees (500 for KICs) at time of investment

- Gross assets within the new thresholds confirmed above

2026 Knowledge-Intensive Company (KIC) Specs

KICs get enhanced investor limits (£2 million annually instead of £1 million) and doubled company caps. They’re typically found in AI, biotech, deep tech, and advanced manufacturing sectors with higher upside potential and longer development horizons. The dividend tax rates context matters for KIC investors comparing EIS returns against income-generating alternatives.

Claiming EIS Tax Relief: The Real Process

Step 1: Invest in an EIS-eligible company

Through EIS funds, crowdfunding platforms, or direct investment. Advance Assurance from HMRC gives some confidence that the company qualifies, but it isn’t a guarantee.

Step 2: Receive the EIS3 certificate

As GOV.UK’s EIS guidance confirms that the company issues the EIS3 certificate (not HMRC) once it’s submitted a compliance statement confirming all conditions have been met for four months post-investment. The EIS3 carries a Unique Investment Reference (UIR).

Don’t lose your UIR. HMRC’s system rejects claims without it, and retrieving it later is a frustrating process that delays your refund.

Step 3: Claim via Self Assessment

Enter the EIS3 details in your Self Assessment tax return or amend a previous year’s return. As GOV.UK confirms, you have up to five years after the 31 January following your investment year to make the claim — so there’s time to plan, but not unlimited time.

Step 4: Use Carry-Back

You can treat a 2026/27 EIS investment as having been made in 2025/26, applying the 30% relief against your previous year’s income tax bill. This is particularly powerful if your 2025/26 income tax exposure was higher, from a bonus, a large dividend distribution, or a property disposal. As noted in the deadline for income tax returns, the timing of when you submit your return affects when carry-back relief can be processed.

EIS vs SEIS vs VCT (2026)

| Feature | EIS | SEIS | VCT |

|---|---|---|---|

| Income tax relief | 30% | 50% | 20% (from April 2026) |

| Max investor annual limit | £1m (£2m KIC) | £200,000 | £200,000 |

| CGT-free growth | Yes (3+ years) | Yes (3+ years) | Yes |

| Loss relief against income | Yes | Yes | No |

| IHT relief potential | Yes (2+ years, BPR) | Yes | No |

| Risk level | Medium-high | Very high | Medium |

SEIS still offers 50% income tax relief — the highest of any UK venture scheme — but limits investors to £200,000 per year and targets truly early-stage companies with significantly higher failure rates. VCT’s rate cut to 20% from April 2026 has materially weakened its position relative to EIS for income tax purposes.

Common Mistakes

Treating EIS as a safe investment. Loss relief reduces the downside but doesn’t eliminate it. A portfolio of genuinely diversified EIS investments is a very different risk profile from a concentrated single startup bet.

Losing the EIS3 or UIR. No paperwork means no claim. Store both the EIS3 certificate and the UIR number in a secure location immediately on receipt.

Ignoring carry-back. One of the most underused strategies in UK tax planning. If last year’s income was higher than this year’s, carry-back can recover more relief than a current-year claim.

Overconcentration. Putting a large EIS allocation into one or two startups concentrates risk in a way that defeats the structure’s purpose. Diversified EIS funds spread exposure across multiple companies within the same tax-efficient wrapper.

2026 Strategy: The Three-Layer Approach

Most experienced EIS investors structure their allocation across three layers:

- Core allocation — a diversified EIS fund offering exposure across eight to fifteen qualifying companies, reducing single-company risk while preserving all the tax reliefs

- High-conviction bet — one or two direct startup investments in sectors where the investor has specific knowledge or deal access

- Tax optimisation layer — carry-back timed to the year with the highest income tax exposure, maximising the value of the 30% offset

This structure captures both the upside potential and the tax efficiency without concentrating risk inappropriately.

EIS Quick Reference (2026)

| Feature | Detail |

|---|---|

| Income tax relief | 30% |

| Max investor annual limit | £1m (£2m for KICs) |

| Company’s annual raise limit | £10m (£20m for KICs) |

| Company lifetime cap | £24m (£40m for KICs) |

| CGT-free gains | After 3 years |

| Loss relief | Against income tax |

| Scheme secured until | 2035 |

| VCT relief (comparison) | 20% from April 2026 |

FAQs

Q. What is EIS tax relief in the UK?

EIS tax relief is a UK government incentive under the Enterprise Investment Scheme that gives investors 30% income tax relief, capital gains tax (CGT) deferral, tax-free growth, and loss relief when investing in qualifying UK companies. It is designed to encourage investment in high-risk, early-stage businesses.

Q. How much EIS tax relief can I claim?

You can claim 30% income tax relief on investments up to £1 million per tax year, or up to £2 million if you invest at least £1 million in Knowledge-Intensive Companies (KICs). You can also carry back any unused relief to the previous tax year.

Q. What changed in EIS from April 2026?

From April 2026, EIS rules were expanded:

- Companies can raise £10 million annually and £24 million lifetime

- Knowledge-Intensive Companies can raise £20 million annually and £40 million lifetime

- VCT tax relief dropped to 20%, while EIS still offers 30%.

The government has extended the scheme until 2035, giving investors greater long-term certainty.

Q. How does EIS loss relief work?

EIS loss relief allows investors to offset losses against income tax if an investment fails. Calculate the loss after deducting the initial 30% income tax relief. For a 45% taxpayer, a failed investment results in an effective loss of about 38.5p per £1 invested, which significantly reduces downside risk.

Q. How do I claim EIS tax relief?

To claim EIS tax relief, you must:

- Receive your EIS3 certificate from the company

- Use the Unique Investment Reference (UIR) provided

- Submit the claim through your Self Assessment tax return or amend a previous return

Claims can also be made online via HMRC.

Q. Can I carry back EIS tax relief to a previous year?

Yes, you can carry back EIS tax relief to the previous tax year. For example, you can apply a 2026/27 investment to your 2025/26 income tax bill, subject to the £1 million annual limit for that year. Investors often use this strategy to reduce past tax liabilities.

Q. Who qualifies for EIS tax relief?

To qualify for EIS tax relief:

- You must be a UK taxpayer

- You cannot be connected to the company (e.g., employee or major shareholder)

- You must hold shares for at least 3 years

- The company must meet EIS eligibility criteria

Q. What is the 3-year rule for EIS?

The EIS 3-year rule requires investors to hold shares for at least three years from the date of issue (or start of trade) to retain tax benefits. Selling early may result in loss of income tax relief and CGT advantages.

Conclusion

EIS tax relief has moved from a niche strategy to mainstream tax planning for high earners in 2026. The company limit increases open access to more established scaling businesses, the VCT rate cut strengthens EIS’s relative position, and the scheme extension through 2035 removes the planning uncertainty that existed before.

The 30% income tax relief, combined with CGT-free growth, loss relief against income, and potential IHT exemption after two years, creates a layered risk-management structure that no other UK investment wrapper currently matches.

Used properly — with diversification, carry-back timing, and the paperwork handled carefully from day one — EIS reshapes what tax-efficient investing looks like for anyone operating above the 40% tax bracket.

For reliable, plain-English guidance on UK tax and personal finance in 2026, Pure Magazine is the resource worth bookmarking.