Every few months, HMRC quietly updates a page on GOV.UK that business owners, landlords, and company directors genuinely dread. It’s called the Deliberate Tax Defaulters list — but most people know it by its more blunt nickname: the HMRC name and shame list.

If your name ends up there, it’s not just a bureaucratic inconvenience. Your full name, address, nature of the tax default, and the penalty amount are visible to anyone with an internet connection — clients, competitors, mortgage lenders, and journalists included. And while HMRC removes the entry after 12 months, the internet has a longer memory than HMRC’s official list. More on that shortly.

So, how does HMRC decide who makes the list? What are the actual thresholds? And critically, what can you do if you’re at risk of appearing on it? This guide covers the complete picture — including how HMRC’s Connect AI system flags landlords before they even know they’re being investigated, why the 30-day representation window is your most important date, and a risk checklist you can use right now.

| Quick Answer: What is the HMRC Name and Shame List? The HMRC name and shame list — officially the Publishing Details of Deliberate Tax Defaulters (PDDD) list — is a public register on GOV.UK. HMRC publishes the names, addresses, and penalty details of people or businesses that have deliberately evaded tax of more than £25,000. To appear, HMRC must determine that the non-compliance was deliberate rather than accidental. Names are published for 12 months before removal from the official list. |

What Is the HMRC Name and Shame List?

The official name is the Publishing Details of Deliberate Tax Defaulters (PDDD) list. It sits on GOV.UK under HMRC’s “corporate reports” section and is updated regularly — typically quarterly — with new entries added and old ones removed after 12 months.

HMRC has operated this scheme since April 2010, following powers introduced under the Finance Act 2009. The policy is explicitly punitive and deterrent: HMRC publishes names not just to penalise the individuals involved, but to signal to other taxpayers that deliberate non-compliance has very public consequences.

As of the most recent 2025 update, the list has included sole traders, company directors, landlords, and business owners — spanning industries from construction and catering to professional services and retail. No sector is exempt, and — importantly — no geography either. While London and the South East see the highest concentration of entries (reflecting population density and the scale of property investment there), defaulters from across the UK appear regularly.

Who Qualifies for the HMRC Name and Shame List?

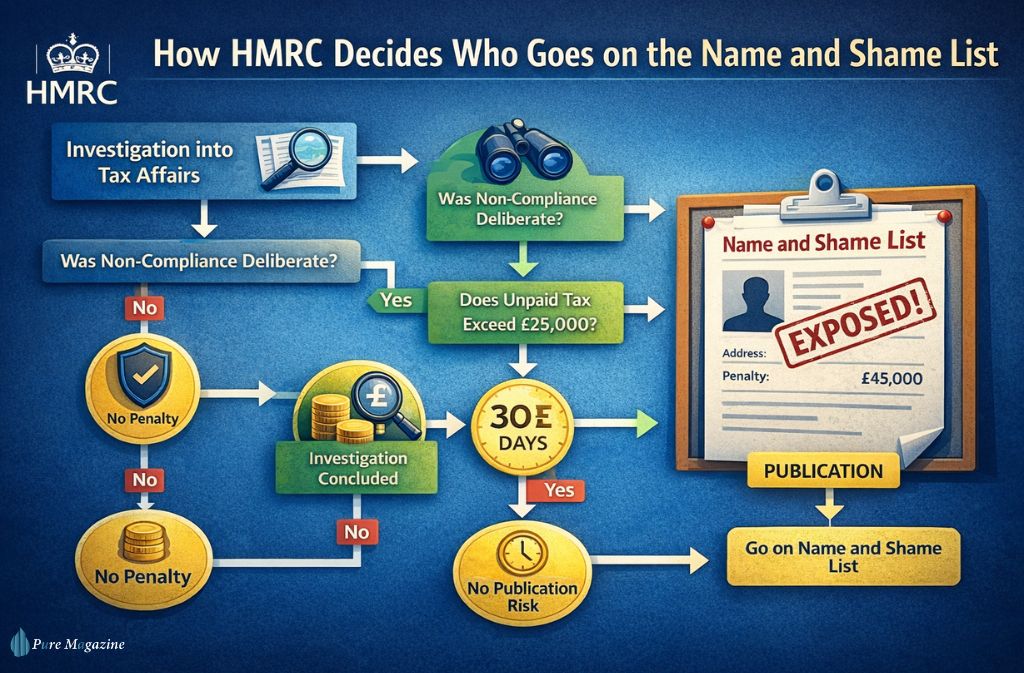

Not everyone who owes HMRC money ends up on the list. The criteria are specific. HMRC must satisfy three conditions before publishing anyone’s details:

Condition 1: The Non-Compliance Must Be Deliberate

HMRC distinguishes clearly between innocent mistakes and deliberate behaviour. A genuine error on your tax return — even a large one — won’t get you named. HMRC is looking for deliberate inaccuracies, deliberate failures to notify HMRC of a liability, or deliberate withholding of information.

In practice, this is where most cases are won or lost. While HMRC claims this standard protects inadvertent errors, the reality — based on how investigations unfold — is that it often catches people who simply panicked and buried their heads in the sand rather than hardened tax criminals. Someone who received rental income, felt guilty, and did nothing is in the same moral category as someone who ran a deliberate fraud. But HMRC’s compliance teams are trained to find the “deliberate” characterisation wherever the evidence allows, because it unlocks both higher penalties and the naming power.

Condition 2: The Unpaid Tax Must Exceed £25,000

There’s a financial threshold. HMRC will only consider naming someone if the amount of tax involved — after investigation and assessment — exceeds £25,000. This applies to the combined total across all relevant taxes, including Income Tax, VAT, Corporation Tax, and PAYE. It is not assessed per tax type separately.

⚠️ Common mistake: The £25,000 is an aggregate figure. If you underpaid £15,000 in Income Tax and £12,000 in VAT, you are over the threshold — even though neither individual amount crosses it alone.

Condition 3: The Investigation Must Be Concluded

HMRC won’t publish your details while an investigation is still open or while you’re in an active appeal. Publication only happens once the matter is settled — either through HMRC’s formal assessment or via tribunal outcome. This means the process from investigation to naming can take months or years, and there are multiple points where the right advice can change the outcome.

What Information Does HMRC Publish?

Once the decision to publish is made, HMRC releases a standardised set of details for each defaulter. As of 2026, this includes:

- Full name (individuals) or trading name and registered address (businesses)

- Nature of the deliberate default (e.g., “deliberate inaccuracies in returns” or “deliberate failure to notify”)

- The tax period(s) involved

- The total amount of tax and penalties assessed

- The taxpayer’s town or county of residence

Names remain on the list for 12 months. After that, HMRC removes them — but removal from GOV.UK is not the same as disappearing from the internet. Data-scraping bots routinely archive the GOV.UK list. A Google search for your name months or even years after removal may still surface a third-party PDF, a news article, or a cached version of the original listing. The reputational footprint outlasts the official record.

How the PDDD Process Works: Step by Step

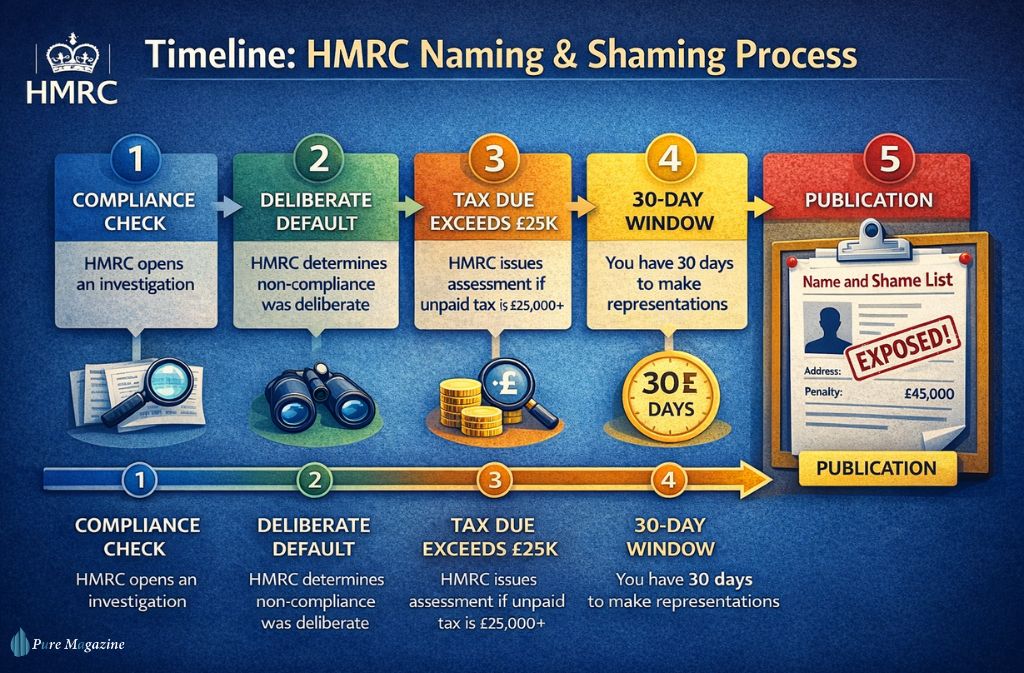

Understanding the process shows you exactly where intervention is possible and where the window closes. Here’s how HMRC moves from suspicion to publication:

- HMRC opens a compliance check or formal investigation into your tax affairs.

- During the investigation, HMRC determines that the non-compliance was deliberate (not careless or innocent).

- HMRC issues a formal assessment for the unpaid tax, plus penalties.

- If the total unpaid tax exceeds £25,000, HMRC notifies you of their intention to publish your details.

- You have 30 days to make representations — this is your formal opportunity to challenge the decision to publish.

- If HMRC proceeds, your details are added to the GOV.UK PDDD list.

- Your name stays live for 12 months, after which HMRC removes it from the current list.

Step 5 is the critical window. Many people don’t realise they have a formal right to challenge publication — and that a well-argued representation can succeed, particularly where there are legitimate grounds to dispute the ‘deliberate’ characterisation. Missing this deadline is not recoverable.

Also Check: Can You Go to Jail for Not Paying Taxes in the UK? (2026)

How HMRC’s Connect System Finds Deliberate Defaulters

One of the most significant developments in HMRC’s enforcement toolkit over the past decade has been the Connect system — an AI-driven data-matching platform that processes over a billion data points from third-party sources every year.

Connect pulls in data from: Land Registry (property ownership and purchase prices), Companies House (directorships and registered addresses), banks and financial institutions (under mandatory reporting rules), DVLA (vehicle ownership), online letting platforms and e-commerce marketplaces, social media and open-source intelligence, and overseas tax authority data under automatic exchange agreements (CRS/FATCA).

In practice, this means Connect can identify a pattern like: person X is registered as director of three companies — their Self Assessment shows modest income — but Land Registry shows they own five properties purchased for a combined £1.2m in the last decade, and a letting platform shows active rental listings. That mismatch creates a risk score that can trigger a targeted compliance check.

For landlords specifically, the Land Registry to Self Assessment cross-reference has been one of the most effective routes to identification. HMRC has publicly confirmed that rental income is a top-three priority for Connect-driven compliance work in 2025–2026. If you own rental property and have not declared the income, the question is not whether HMRC will find it — it’s when.

HMRC Name and Shame List vs. Other HMRC ‘Naming’ Schemes

The PDDD list is just one of several HMRC naming schemes. It’s easy to confuse them, and the consequences are different for each.

| Scheme | What It Covers | Threshold | Duration on List |

| PDDD (Name & Shame) | Deliberate tax defaulters | £25,000+ unpaid tax | 12 months |

| National Minimum Wage | Employers underpaying NMW | Any underpayment | Listed on publication date |

| Tax Avoidance Scheme Promoters | Promoters of notified schemes | HMRC-registered scheme | Until scheme closed |

| HMRC Avoidance List | Active avoidance schemes (not individuals) | HMRC-flagged | Until scheme resolved |

If you’re a landlord or self-employed contractor, the PDDD list is the one most directly relevant to you. Employers should also monitor the National Minimum Wage publication list separately — it operates under entirely different criteria and covers much smaller amounts.

Common Reasons People End Up on the HMRC Name and Shame List

Based on patterns in published PDDD data, the most frequent categories of default include:

- Deliberately understating income on Self Assessment returns

- Claiming VAT repayments on fictitious or inflated invoices

- Failing to register for VAT despite trading above the threshold

- Operating shadow payroll or failing to account for PAYE on cash wages

- Submitting corporation tax returns with deliberately misstated figures

- Buy-to-let landlords failing to declare rental income over multiple years

Landlords have featured prominently in recent PDDD publications. The construction sector and cash-in-hand trades (catering, cleaning, personal services) have also been disproportionately represented. London and the South East account for the largest share of entries, though this reflects the volume of self-employment and property investment activity in those regions rather than any deliberate geographic targeting by HMRC.

Also Read: HMRC Business Tax Account 2026: Complete Step-by-Step Guide

2026 Update: What’s Changed with HMRC’s Naming Policy?

HMRC’s enforcement posture has shifted noticeably over the past two years. Several developments are worth knowing as of 2026:

Connect Is Getting Better — And Faster

The Connect system’s data sources have expanded to include more granular letting platform data, overseas property ownership via international exchange agreements, and improved e-commerce income tracking. Investigations that previously took 18–24 months from identification to compliance check are being completed faster as Connect’s risk-scoring becomes more refined.

Landlords Remain a Priority Target

HMRC has maintained rental income as a top-three compliance priority for 2025–2026. The Let Property Campaign — HMRC’s voluntary disclosure route for landlords — remains open, and HMRC has been explicit that those who use it will not generally be subjected to PDDD publication. Those who don’t and are subsequently investigated face significantly higher penalties and the risk of naming.

To make a voluntary disclosure under the Let Property Campaign: visit gov.uk/let-property-campaign, complete the online notification, and HMRC will provide a calculation period (typically 90 days) to submit your disclosure. Engaging a specialist for this process is advisable if the amounts involved are substantial.

Penalty Regime Unchanged for 2026

The penalty percentages for deliberate non-compliance have not changed for 2026. Deliberate but not concealed defaults attract penalties of 20–70% of unpaid tax (domestic) or 30–70% (offshore). Deliberate and concealed behaviour attracts 30–70% (domestic) or 50–200% (offshore). These sit on top of the unpaid tax itself.

The ‘Permanent’ Digital Footprint: A 2026 Warning

Do not assume that ‘12 months’ means the record disappears entirely. In 2026, data-scraping bots routinely archive the GOV.UK PDDD list. Even after HMRC removes the official entry, a Google search for your name may still surface a third-party PDF, a cached version, or a news article covering the original publication. Specialist reputation management services exist for this, but prevention remains the only reliable solution.

There is also the question of financial services. While HMRC removes the name after 12 months from their own list, third-party “risk intelligence” databases used by banks, insurers, and mortgage lenders — including platforms like World-Check — may retain the record far longer. This can affect future mortgage applications, business banking relationships, and professional indemnity insurance, sometimes years after the HMRC entry has gone.

Director’s Liability: An Overlooked Consequence

For company directors, appearing on the PDDD list carries a risk beyond reputational damage. HMRC works closely with the Insolvency Service, and a finding of deliberate tax default can form part of the grounds for disqualification proceedings under the Company Directors Disqualification Act 1986 (CDDA).

Disqualification prevents a person from acting as a company director for a period of 2–15 years. The conduct threshold under the CDDA is lower than you might expect — “unfit conduct” includes failing to ensure a company meets its tax obligations where the director knew of the liability and took no action. A PDDD finding is powerful evidence of exactly that.

This is not a theoretical risk. HMRC routinely passes PDDD case information to the Insolvency Service’s investigations team. If you are a director of a limited company and your default relates to company taxes, this is a consequence that should be factored into any legal strategy from the outset.

Also Read: Tax Identification Number UK: What It Is & How to Find It (2026)

5 Mistakes That Increase Your Risk of Being Named

Most people who end up on the HMRC name and shame list didn’t plan to be there. These are the patterns that consistently increase risk:

- Mistake 1: Treating HMRC’s inaction as permission. HMRC can carry out retrospective investigations covering up to 20 years where deliberate behaviour is suspected. Silence from HMRC is not clearance.

- Mistake 2: Making partial disclosures. If you voluntarily disclose some income but omit other sources, and HMRC later discovers the omission, the voluntary character of your disclosure is undermined — and the ‘deliberate’ finding becomes much easier for HMRC to establish.

- Mistake 3: Not getting professional representation early enough. The 30-day window to make representations against HMRC’s intention to publish is tight. Having the right adviser briefed before that window opens is the difference between a successful challenge and a missed deadline.

- Mistake 4: Assuming the £25,000 threshold is per-tax. It is not. HMRC aggregates the total across all taxes in the investigation.

- Mistake 5: Ignoring HMRC’s nudge letters. If you’ve received a letter from HMRC suggesting you review your tax affairs, that is a pre-enforcement signal. Ignoring it and being formally investigated later makes a deliberate finding significantly more likely.

What To Do If You’re at Risk of Appearing on the List

If you believe you may be under investigation, or you know your tax affairs have gaps that HMRC might characterise as deliberate, your options are not as limited as they might seem.

Option 1: Voluntary Disclosure

HMRC runs several formal disclosure facilities. The Let Property Campaign covers rental income (gov.uk/let-property-campaign). The Worldwide Disclosure Facility covers offshore income (gov.uk/guidance/use-the-worldwide-disclosure-facility-to-make-a-disclosure). Voluntary disclosure before HMRC opens a formal investigation typically results in lower penalties and — critically — removes the naming risk almost entirely.

Option 2: Challenge the ‘Deliberate’ Finding

If an investigation is already underway, the most important ground to contest is the characterisation of your behaviour as ‘deliberate’ rather than careless or innocent. This is a facts-and-evidence argument that requires specialist tax investigation expertise — not just a general accountant. The distinction between ‘deliberate’ and ‘careless’ is both legally significant and genuinely contestable in many cases.

Option 3: Representations Against Publication

Even where HMRC has reached a deliberate finding and the threshold is met, you have a formal 30-day right to make representations against the naming decision itself. Grounds include: procedural errors in HMRC’s process, disproportionality arguments, and cases where publication would cause undue harm to third parties (for example, employees of a named business).

Also Read: Council Tax Moving House: What You Must Do (2026 Guide)

Support if You’re Under Investigation

A serious HMRC investigation is not just a financial problem. The stress of an ongoing compliance check or criminal investigation can be significant, and the impact on sleep, relationships, and mental health is well-documented. If you are finding the pressure difficult to manage, two organisations are worth knowing about:

- TaxAid (taxaid.org.uk) — a charity offering free, confidential tax advice to people on lower incomes who cannot afford professional representation. They have specialist knowledge of HMRC processes and can provide a degree of practical support even in complex cases.

- Your GP or a mental health professional — if the anxiety is affecting your daily functioning. HMRC investigations can last months or years, and sustainable management of the process matters.

There is no shame in acknowledging that HMRC’s enforcement machinery is a stressful thing to navigate. Getting the right professional advice — and the right personal support — are both legitimate and important responses.

Can You Search the HMRC Name and Shame List?

Yes. The current PDDD list is publicly accessible on GOV.UK. The list is structured as a table with entries removed on a rolling 12-month basis. There is no official archived historical database maintained by HMRC — once 12 months expire, the entry leaves the official list. But as noted above, third-party archives may retain records beyond that point.

Case Study: How “Mr. A” Almost Ended Up on the List (and Didn’t)

Mr A — a landlord in the South East — owned four buy-to-let properties and had not declared rental income for six years, accounting for approximately £42,000 in unpaid Income Tax. He knew about the income. He’d told himself he’d sort it out next year, every year, until the years added up.

The letter from HMRC arrived in early 2024 — a ‘nudge letter’ flagging a mismatch between Land Registry records and his Self Assessment returns. Mr. A’s first instinct was to ignore it and hope it went away. His second instinct — thankfully — was to call a tax investigation specialist.

The specialist advised making an immediate voluntary disclosure under the Let Property Campaign. The disclosure was accepted. Penalties were charged at the lower ‘prompted disclosure’ rate of 30% rather than the maximum 70% that would have applied had HMRC opened a formal investigation first. HMRC confirmed in writing that the PDDD publication was not being pursued.

Total cost: £42,000 in unpaid tax, £12,600 in penalties, plus professional fees. Substantial — but nothing close to the reputational and commercial cost of 12 months named on a public list, plus the potential for mortgage lender and banking complications that could have followed.

The moment he received the nudge letter was also, it turned out, the last moment the voluntary route was cleanly available. A few months later, after a formal investigation opened, the calculation would have looked very different. That timing matters.

Also Check: Dividend Tax Rates UK 2026: What’s Changing and What You’ll Pay

Conclusion

The HMRC name and shame list is a genuine enforcement tool with real consequences: 12 months of public visibility for your name, address, and the details of your tax default — plus a digital footprint that may outlast the official entry. It applies to deliberate defaulters who owe more than £25,000 in aggregate, and HMRC’s ability to identify candidates has grown substantially as the Connect system matures.

The practical takeaways: the threshold is lower than most people assume and it aggregates across taxes; voluntary disclosure before a formal investigation almost always forecloses the naming route; the 30-day representation window is your last formal line of defence once an investigation concludes; and directors face an additional disqualification risk that is often overlooked.

If you have undisclosed income or gaps in your tax affairs, acting voluntarily is almost always the better outcome. The hmrc name and shame list is designed precisely to change the risk calculus for those who are waiting to see what happens. Now you know what happens.

FAQs

Q. Can HMRC publish the names of tax evaders?

Yes. Under the Finance Act 2009, HMRC has the legal power to publish details of individuals and businesses who deliberately evade tax above £25,000. This is the basis for the PDDD list, updated quarterly on GOV.UK.

Q. How long do names stay on the HMRC name and shame list?

Names remain on the official HMRC deliberate tax defaulters list for 12 months from the date of first publication. After that, HMRC removes them from the current list. However, third-party archives, risk intelligence databases used by banks, and cached search results may retain the information beyond that point.

Q. What is the minimum amount of tax you need to owe to appear on the list?

The threshold is £25,000 in unpaid tax, aggregated across all taxes involved in the investigation — Income Tax, VAT, Corporation Tax, PAYE — not assessed per tax type separately. Someone who underpaid £15,000 in Income Tax and £12,000 in VAT is over the threshold.

Q. Can HMRC chase a 10-year-old debt?

In most cases, HMRC has a 4-year window to raise assessments for careless errors and a 6-year window for deliberate behaviour. Where deliberate concealment is suspected, HMRC can go back 20 years. Old debts can absolutely resurface — and if the total exceeds £25,000 and HMRC deems the behaviour deliberate, naming is still on the table.

Q. Does HMRC name people who use legal tax avoidance schemes?

The PDDD list covers deliberate tax evasion, not legal avoidance. However, HMRC separately publishes a list of tax avoidance scheme promoters and active schemes under different legislation. Using a disclosed avoidance scheme won’t put you on the name and shame list, though HMRC does publicly identify those schemes via a separate register.

Q. How can I avoid appearing on the HMRC name and shame list?

The most effective route is voluntary disclosure before HMRC opens a formal investigation. HMRC’s Let Property Campaign (for landlords) and Worldwide Disclosure Facility (for offshore income) both allow taxpayers to correct their records at reduced penalty rates. HMRC has confirmed it will not generally name voluntary disclosers on the PDDD list.

Q. What is the HMRC snitch scheme?

This refers to HMRC’s fraud reporting service, which allows the public to report suspected tax fraud. Reports can trigger compliance investigations. The reporting route is separate from the PDDD publishing process — a report doesn’t directly result in naming, but it can initiate the investigation that eventually leads there.

Q. Can appearing on the HMRC list affect your ability to get a mortgage?

Potentially, yes. While HMRC removes the official entry after 12 months, third-party risk intelligence databases used by lenders — including platforms like World-Check — may retain the record longer. Some lenders conduct enhanced due diligence checks that include these databases. If you are planning a mortgage application, it is worth understanding whether your name appears in any third-party risk registers, not just the live HMRC list.

Appendix: Quick-Reference Risk Checklist

Use this to assess your exposure to the PDDD naming regime:

| Risk Factor | Higher Risk | Lower Risk |

| Income declaration | Gaps or known omissions in returns | All income declared and reconciled |

| Disclosure history | No prior disclosures to HMRC | Previous voluntary disclosures made |

| HMRC contact | Received nudge letter or compliance check | No HMRC contact outside routine |

| Tax owed (estimated) | Above £25,000 across all taxes | Below £25,000 total |

| Nature of error | Knew about it and did nothing | Genuine misunderstanding or adviser error |

| Director status | Director of company with undisclosed tax | Not a director or tax position clean |

| Property ownership | Rental property with undeclared income | No rental income or fully declared |

If two or more “Higher Risk” boxes apply to you, the prudent step is to seek specialist tax investigation advice before HMRC makes contact.

Related: Tax Deduction at Source UK: PAYE Explained for 2026