Nobody wakes up thinking they will be defrauded today. That is part of why it keeps working.

Fraud has been around as long as money itself, but the version that exists in 2026 is something different. It is faster, more convincing, and harder to trace. The FBI’s Internet Crime Complaint Center put global cyber-fraud losses at over $12.5 billion in 2024 — and that figure only counts what was actually reported. The real number is almost certainly higher, because embarrassment and confusion stop many victims from ever filing a complaint.

When someone does fall victim, there is a specific word for them in legal and financial contexts: a fraudee. It sounds clinical, almost detached. But it describes something that happens to real people every single day — people who were not careless, not unintelligent, just targeted by someone very good at deception.

This guide unpacks what the term means, how fraud actually plays out in practice, and — most importantly — what people can do to protect themselves.

So What Exactly Is a Fraudee?

A fraudee is simply the victim of fraud. That means any person, company, or organization that suffers a lose someone intentionally deceived them to steal money, gain access to accounts, or extract sensitive information.

The legal definition of fraud is built around four elements that all have to be present at the same time:

- A false statement or misrepresentation of facts

- The person making it knows it is false

- The intention is to deceive

- The victim suffers actual harm as a result

Take away any one of those elements, and it may not legally qualify as fraud — though courts and regulators in different countries apply their own standards. What matters practically is the last point: the fraudee ends up worse off than before they encountered the fraudster.

A straightforward example: a scammer sends an email pretending to be a major bank, complete with logos and official-looking language. The recipient enters their password on a fake login page. The scammer empties the account. The bank did nothing wrong. The recipient was not stupid. They were targeted, deceived, and became the fraudee.

The Most Common Ways People Become Fraudees

Fraud does not announce itself. It tends to arrive disguised as something familiar — a bill, a job offer, a love interest, an urgent phone call from a relative. The specific forms it takes are worth understanding, because recognising the shape of a scam before it is too late is the entire game.

Identity Theft

Personal information is remarkably valuable on criminal markets. Social security numbers, passport details, banking credentials, and even combinations of name, address, and date of birth can be used to open new accounts, apply for loans, or file fraudulent tax returns — all in someone else’s name. Identity theft victims frequently do not realize anything has happened until a debt collector calls, or their mortgage application is rejected over a credit score that has been quietly destroyed.

Credit Card Fraud

Card fraud is one of the oldest tricks in the book, but the methods have multiplied. Skimming devices on ATMs, large-scale retailer data breaches, phishing emails designed to harvest payment details, and even shoulder surfing in busy cafes are all common routes. The first sign is usually a transaction the account holder does not recognize — sometimes for a small, almost forgettable amount that the fraudster uses to test whether the card is still active before making a larger move.

Investment Scams

These target ambition as much as greed. The pitch is usually something plausible — a cryptocurrency opportunity with strong early returns, a private investment fund with a glossy prospectus, a trading platform that seems to perform suspiciously well. Victims often watch their “account balance” grow for weeks before trying to withdraw funds and discovering the money was never real. The

U.S. Securities and Exchange Commission maintains a publicly searchable database of registered investment advisers and known scams at investor.gov — a useful first stop before putting money into anything unfamiliar.

Romance Scams

Probably the most psychologically damaging form of fraud. A stranger makes contact — usually on a dating app or social media — and invests weeks or months building a relationship. The conversations feel real. The affection feels genuine. Then a crisis appears: a medical emergency, a legal problem, travel complications. Money is requested. More money follows. By the time the victim starts questioning things, they may have transferred their savings to someone who was never who they claimed to be. According to the FTC, romance scams cost Americans over $1.3 billion in 2023 alone.

Online Marketplace Fraud

Buying and selling online has become second nature for most people, which makes it an obvious hunting ground. Fake listings for products that do not exist, rental properties that belong to someone else, counterfeit goods shipped at full price — these are all routine. Payment is made, the seller disappears, and the buyer is left with nothing but a transaction receipt that leads nowhere.

AI Voice and Deepfake Scams — The 2026 Threat

This one deserves special attention because it has changed what fraud looks like entirely. Using a few seconds of audio scraped from a social media post, AI tools can now generate a convincing replica of almost anyone’s voice. Victims receive a phone call that sounds exactly like their child, their parent, or their boss — often in a state of panic, asking for urgent money. Some have received video calls featuring deepfake versions of people they trust. This is not a future risk. It is happening right now, and the technology is only getting more accessible.

Why Intelligent People Get Caught Out

There is a persistent and unhelpful assumption that fraud only catches people who are naive or inattentive. The reality is more uncomfortable. Fraud is fundamentally a psychological exercise, not a technical one, and the tactics used are specifically designed to override critical thinking.

Urgency is probably the most effective weapon in the fraudster’s toolkit. When someone is told their account will be suspended in two hours, or that a relative is in danger and needs money immediately, the normal instinct to pause and verify gets short-circuited. The brain shifts into problem-solving mode and stops asking whether the situation is real.

Authority works similarly. An email that appears to come from a government agency, a bank, or a senior manager triggers a kind of automatic compliance in most people. Questioning authority feels uncomfortable, especially when the communication looks official.

Fear, emotional manipulation, and exploitation of trust are all layered on top of these. Combine them skillfully — as experienced fraudsters do — and the result can fool people with advanced degrees, professional backgrounds, and years of experience navigating complex environments.

Knowing this does not make anyone immune. But it does shift how seriously people take the warning signs when they appear.

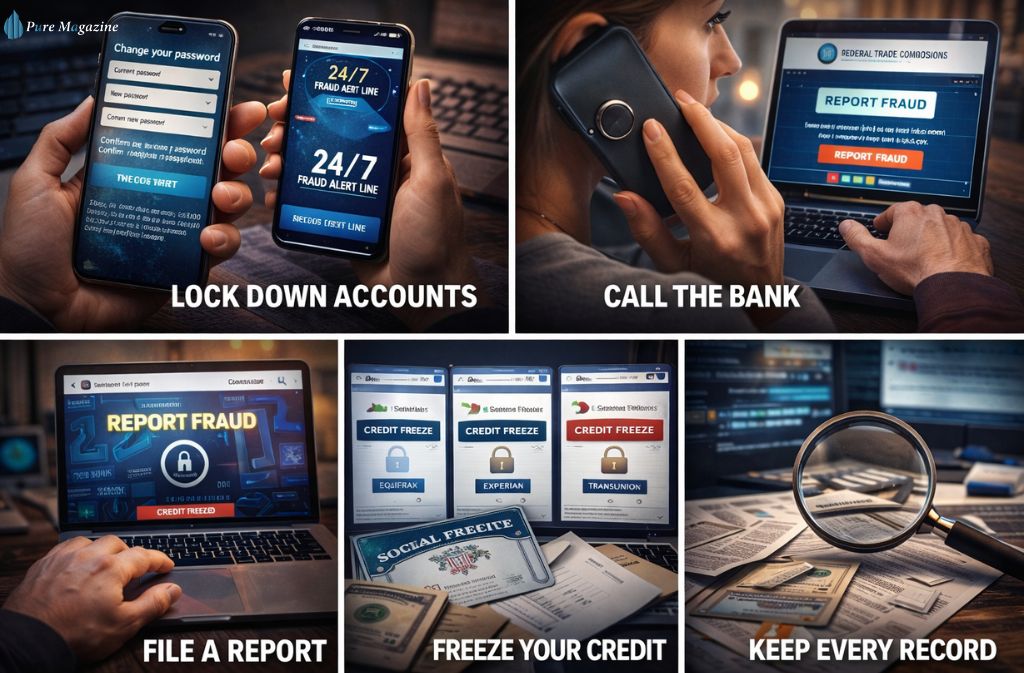

What to Do the Moment You Realise Something Is Wrong

Speed is everything here. The faster a fraud victim responds, the better the chances of limiting the damage — and in some cases, recovering lost funds.

Lock Down Accounts First

Change passwords immediately on any account that may have been compromised. Enable two-factor authentication if it is not already on. Log out of active sessions on devices that are not recognized. If there is any chance a device itself has been compromised, treat everything on it as potentially exposed.

Call the Bank Without Delay

Most financial institutions have 24-hour fraud lines precisely for this reason. A quick call can freeze a card, halt a transfer that has not yet cleared, or flag the account for monitoring. The window for recovering an outbound transfer is narrow — often just hours — so waiting until morning is rarely a good idea.

File a Report

In the United States, fraud reports can be filed directly with the FTC at reportfraud.ftc.gov. UK residents can report to Action Fraud. These reports rarely result in immediate action, but they contribute to patterns that investigators use to pursue larger operations — and they create an official record that can help with insurance claims or bank disputes.

Put a Freeze on Credit

If personal information was compromised, placing a credit freeze with the major bureaus prevents new accounts from being opened in the victim’s name. In the US, this can be done for free directly with Equifax, Experian, and TransUnion. It is one of the most effective tools available and takes only a few minutes to set up.

Keep Every Record

Screenshots, emails, transaction histories, phone records — all of it. Even things that seem trivial at the time. Documentation matters enormously when dealing with banks, insurers, or law enforcement, and it is much harder to reconstruct after the fact.

Practical Ways to Avoid Becoming a Fraudee

Most fraud prevention advice sounds obvious in hindsight. The challenge is applying it consistently, especially when people are busy, distracted, or dealing with something that appears legitimate.

A few habits make an outsized difference:

- Multi-factor authentication on every account that offers it — email, banking, social media, everything

- A password manager, because reused passwords are one of the most common entry points for account takeovers

- Verifying any unexpected request for money or personal information through a separate channel — if someone calls claiming to be from a bank, hang up and call the number on the back of the card

- Treating urgency as a red flag rather than a reason to act faster

- Checking financial statements at least once a week, not just at the end of the month

- Being thoughtful about what personal details are publicly visible on social media

Quick Reference: What to Do in Common Scenarios

| Situation | First Action |

| Unauthorized bank transaction | Call the bank immediately |

| Suspected identity theft | Freeze credit with all three bureaus |

| Paid for an item that never arrived | Report to payment provider and marketplace |

| Clicked a suspicious link | Change passwords, run a malware scan |

| Received a convincing scam call | Hang up, verify directly, report to FTC |

How Fraud Is Changing in 2026

The fraud landscape shifts every year, but 2026 has brought a few developments that are worth paying close attention to.

Artificial intelligence has handed fraudsters a set of tools that would have seemed far-fetched five years ago. Voice cloning, deepfake video, and AI-generated phishing emails that are grammatically flawless and personally tailored — these are no longer experimental. They are in active use. The badly spelled email from a Nigerian prince has been replaced by something that reads like it was written by a careful, attentive colleague.

Data breach exploitation has also become more sophisticated.

When a large company is breached, the stolen records do not just get dumped on a dark web forum and forgotten. Instead, criminals cross-reference them with other databases and enrich them with additional details. They use this information to craft attacks that reference real account information, recent activity, and personal details that only a legitimate institution should know.

This makes the standard advice — “your bank will never ask for your password” — harder to follow. Fraudsters can already know the last four digits of the account and the most recent transaction.

Social engineering, meanwhile, remains the most reliable method of all. No malware required, no technical skill necessary — just patience, a convincing cover story, and the ability to read how a person is responding. Organizations in particular have found this to be a growing problem, as staff at all levels can become entry points if they are not trained to recognize the signs.

Closing Thoughts

Fraud is one of those risks that people tend to think about in the abstract — something that happens to other people, in other circumstances. The statistics suggest otherwise. It crosses income levels, age groups, professions, and countries without much discrimination.

Understanding what a fraudee is, and how the process of becoming one actually works, matters because it changes how people approach their own behavior. Not with paranoia, but with a clear-eyed awareness that deception is a skill that some people have spent years refining. And that the best counter to it is knowing what to look for before it happens.

Quick reporting can limit financial loss. Strong digital habits reduce exposure. And treating any unexpected request for money or personal information with a moment of deliberate skepticism costs nothing at all.

In a world where anyone can generate a convincing deepfake in minutes and personalize a phishing email using publicly available data, staying skeptical is your most valuable tool.

Related: FBI Warns iPhone Android Scams: Stay Safe from Mobile Fraud