A tax code change can trigger instant anxiety. The letter from HM Revenue & Customs has landed. Your payslip looks different. The number 1257L disappears, and the 1131N tax code appears instead.

It feels technical. Slightly ominous.

In reality, the 1131N tax code is usually linked to Marriage Allowance — but in 2026, frozen thresholds, fiscal drag, and side incomes mean the implications are more nuanced than most guides explain.

This is not just a definition. This is what it means for your household, your eligibility, and your take-home pay — now.

What the 1131N Tax Code Actually Means (2026 Rules)

The 1131N tax code breaks down like this:

- 1131 → You have £11,310 of tax-free income this tax year

- N → You have transferred 10% of your Personal Allowance to your spouse or civil partner under Marriage Allowance

The standard Personal Allowance remains £12,570 (frozen until at least 2028). Marriage Allowance allows a transfer of £1,260 (10%).

£12,570 – £1,260 = £11,310. Drop the final zero → 1131. That’s the code.

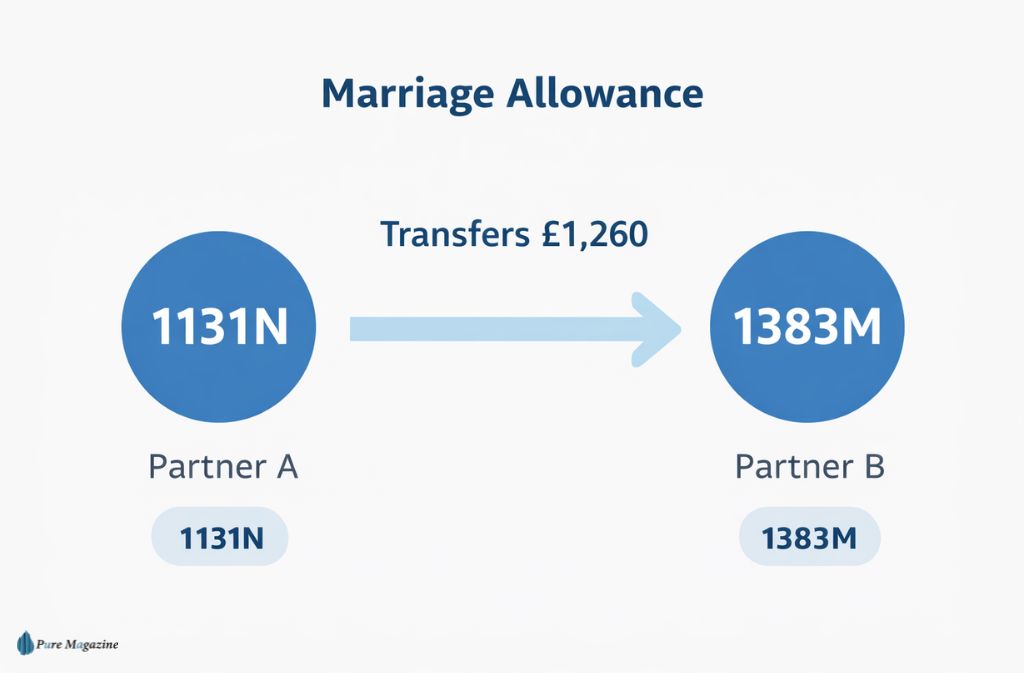

But here’s the key: 1131N never exists in isolation. It almost always appears as part of a partner pair.

The “Partner Pair” Rule: If You Have 1131N, Your Partner Has 1383M

Marriage Allowance works like a relay baton — one partner gives, the other receives.

If one partner’s code is 1131N, the other’s is usually 1383M.

| Partner Role | Tax Code | Personal Allowance | What It Signals |

|---|---|---|---|

| Lower earner (giver) | 1131N | £11,310 | Transferred £1,260 |

| Basic rate earner (receiver) | 1383M | £13,830 | Received £1,260 |

The “M” stands for “Married — received transfer.” The “N” stands for “Married — given transfer.”

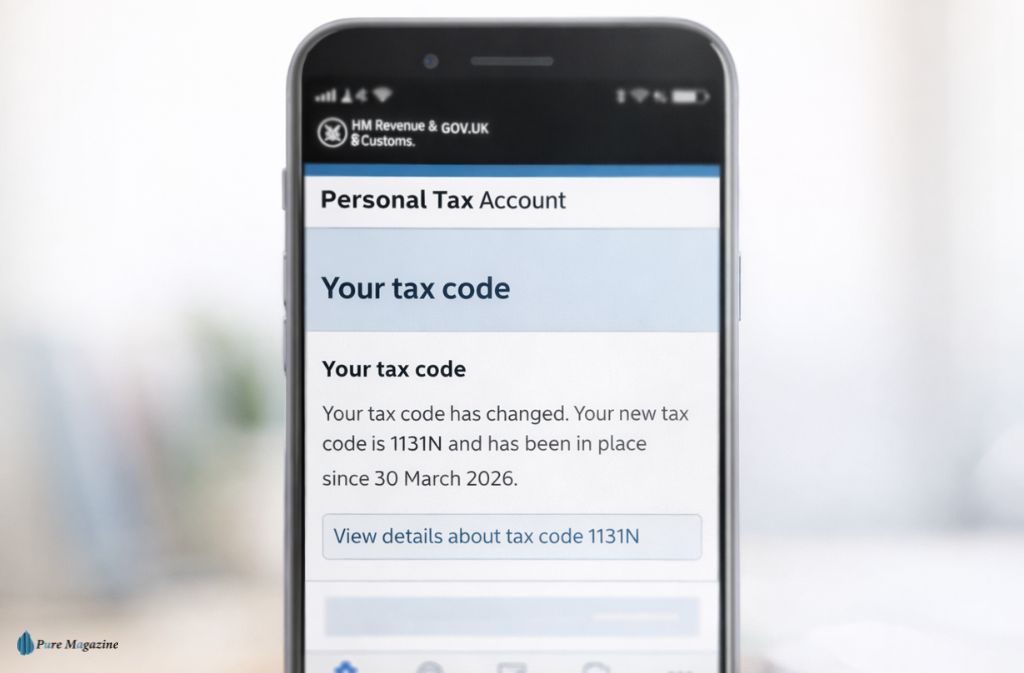

Why 1257L Changed to 1131N

If your code moved from 1257L to 1131N, one of these happened:

- Marriage Allowance was successfully claimed

- HMRC processed a delayed approval

- Your partner applied and included you

- A previous claim was reinstated

You can verify this inside your Personal Tax Account on GOV.UK or through the HMRC app.

For most couples, this change increases total household income by up to £252 per year.

But in 2026, there’s a catch.

The 2026 Income Cap Warning (Fiscal Drag Risk)

Marriage Allowance only works if the receiving partner is a basic rate taxpayer and earns below £50,270 (England/Wales/Northern Ireland threshold).

Because this threshold has been frozen, inflation-driven pay rises are quietly pushing more people into the higher rate band — a phenomenon known as fiscal drag. Understanding what the 40% tax bracket triggers and at exactly what income level it applies is critical for couples where the receiving partner’s earnings are creeping upward.

If your partner’s income creeps above £50,270:

- They are no longer eligible

- Marriage Allowance should stop

- 1131N may become incorrect

Many couples miss this. Small raise. Unexpected disqualification.

If your partner earns over £50,270 in 2026, pause and check immediately.

Scottish Taxpayers: Watch for S1131N

If you live in Scotland, your code may begin with an “S”: S1131N.

Scotland has different tax bands (Starter, Basic, Intermediate, Higher). The eligibility rule still depends on whether the receiving partner remains within the appropriate basic-rate equivalent band.

Because Scottish thresholds differ slightly, borderline cases are more common. Always confirm band positioning rather than assuming eligibility continues automatically.

How 1131N Affects Take-Home Pay

Let’s ground this in reality.

The lower earner earns £10,000. The higher earner earns £30,000. Lower earner transfers £1,260.

Result:

- Lower earner’s allowance drops to £11,310

- Higher earner’s allowance increases to £13,830

- Household saves up to £252 annually

Individually, the lower earner may feel a slightly earlier tax trigger if their income rises above £11,310. But overall, the household benefits.

Marriage Allowance is designed for household efficiency — not individual maximisation. An after-tax calculator can help you model exactly what your combined take-home looks like before and after the transfer.

Side Hustles & Second Jobs: Where Confusion Starts

In 2026, more people have freelance income, Etsy or Shopify sales, consulting side work, or rental income.

Here’s how the 1131N tax code interacts:

- Your Personal Allowance is usually applied to your main PAYE job only

- A second job may use BR (20% flat) or 0T

- Self-employed income is assessed via Self Assessment

If your combined income exceeds your allowance unexpectedly, you may owe tax later — even with 1131N applied correctly. Marriage Allowance does not override second-job mechanics. It simply adjusts the allowance split.

Frozen Personal Allowance: The Real 2026 Insight

The Personal Allowance has been frozen at £12,570 for years. The Marriage Allowance saving — capped at £252 per year — has also effectively been frozen.

Inflation reduces the real value of that saving every year.

In other words, the nominal benefit remains £252. The real-world purchasing power shrinks.

This doesn’t mean the Marriage Allowance is pointless. It means expectations should be realistic. For a fuller picture of when the personal tax allowance might increase, the freeze and its political context are worth understanding.

Backdating: The Overlooked Opportunity

Here’s where many couples leave money on the table.

As confirmed on GOV.UK’s Marriage Allowance guidance, you can backdate your claim to 6 April 2021 (the 2021 to 2022 tax year) for any years you were eligible. Your partner’s tax bill will be reduced depending on the Personal Allowance rate for the years you’re backdating.

That could mean £252 × 4 = £1,008 potential backdated refund (depending on historical allowance values).

Many people discover 1131N and only think forward. The real question is: were you eligible before you applied? If yes, a backdated claim may trigger a lump-sum repayment.

When 1131N Could Be Wrong

Even though it’s usually accurate, mistakes happen. Check immediately if:

- Your partner now earns above £50,270

- You are separated or divorced

- You became the higher earner

- You started earning above £12,570 yourself

- You never knowingly applied

Incorrect codes can lead to underpayment or overpayment — neither is pleasant at tax year reconciliation time. If you suspect your code is wrong, checking your tax code through HMRC’s official system allows you to review what HMRC is currently using and update it if needed.

Quick Self-Check Logic

Use this simple framework:

Step 1: Does your partner earn under £50,270? If no → Stop. Code may be wrong.

Step 2: Do you earn under £12,570? If yes → Transfer makes sense.

Step 3: Are you still legally married or in a civil partnership? If no → Cancel immediately.

If unsure, check via HMRC online services.

How to Cancel or Adjust 1131N

You can cancel Marriage Allowance online, update income estimates, notify changes in marital status, or call HMRC directly.

Changes typically reflect in payroll within weeks. If tax was overpaid, it is usually corrected via PAYE adjustment or refund. Any unclaimed tax refund resulting from an overpayment due to an incorrect 1131N code can be recovered through your personal tax account.

Common Misunderstandings

“1131N means I’m taxed more.” Not exactly. It means your allowance is lower because part was transferred.

“It applies automatically when you marry.” No. An application must be made.

“It reduces household income.” Generally false — unless eligibility is breached and not corrected.

Why Understanding 1131N Matters in 2026

Tax codes used to feel static. Now they shift more frequently because of digital HMRC adjustments, job mobility, side incomes, and frozen thresholds.

Small letters. Real consequences.

Understanding your tax code prevents surprise underpayments — and avoids leaving legitimate savings unclaimed. Those who have previously dealt with a wrong tax code know how quickly an overlooked letter can translate into an unexpected bill or a missed refund.

FAQs

Q. What does 1131N tax code mean?

1131N means you have transferred 10% of your Personal Allowance (£1,260) to your spouse or civil partner under Marriage Allowance, reducing your tax-free income to £11,310.

Q. Why did my tax code change from 1257L to 1131N?

It changed because the Marriage Allowance was applied. Your Personal Allowance was reduced and the “N” suffix added to indicate you transferred part of it. For a full explanation of what the standard 1257L tax code means and why it’s the default starting point, that context helps clarify exactly what changed.

Q. What is the partner’s tax code if mine is 1131N?

Your partner’s code is usually 1383M, showing they received the transferred allowance.

Q. Can I backdate a Marriage Allowance claim?

Yes. As confirmed on GOV.UK, you can typically backdate up to four previous tax years if eligibility requirements were met in those years.

Q. What happens if my partner earns over £50,270?

Marriage Allowance no longer applies. The 1131N tax code may become incorrect and should be updated. Check your income tax bands to confirm exactly where your partner’s earnings now sit.

Final Words

The 1131N tax code is not a penalty. It’s a strategic transfer.

But in 2026 — with frozen allowances, fiscal drag, and multiple income streams — eligibility can shift quietly.

A quick review now can prevent problems later.

Check the pair. Check the threshold and history.

Tax codes are small details that control real money.

Good financial decisions depend on current, accurate information. That’s exactly what Pure Magazine delivers — across tax, savings, income, and beyond.